What Is It and What Does It Cover?

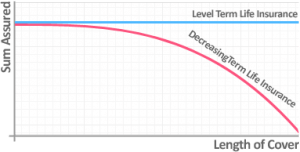

Decreasing Term Life Insurance is a form of Life Insurance which reduces over time paying out a cash lump sum benefit should the policyholder die. This makes it particularly suitable for covering an outstanding repayment mortgage, where the figure you owe also falls over time.

- It pays out a tax free cash lump sum on death.

- The figure you’re insured for falls over the ‘term’ of the insurance in line with an outstanding debt such as a mortgage.

- It provides you with peace of mind knowing those closest to you will be financially secure should you pass away.

- Option to include Critical Illness Insurance to provide a cash lump sum should you suffer a serious illness, such as cancer, heart attack or stroke.

How Does Decreasing Life Insurance Work?

If you were to take out a policy worth £200,000 for 25 years and had a mortgage term for the same length of time, the policy’s benefit and your debt would gradually decrease until the end of the policy and mortgage term where they would both equal zero.

Should you pass away at any point during the mortgage, the level of cover provided by the reducing life insurance would be enough to pay off the outstanding debt. Decreasing Life Insurance is the most cost effective way of protecting a repayment mortgage.

![life insurance decreasing cover graph]()

What About Protecting An Interest Only Mortgage?

If you are looking to protect an interest-only mortgage or are simply looking for a level of cover which is fixed over the life of the plan then a more suitable option may well be Level Term Life Insurance.

If you were to set-up a Level Life Insurance policy covering £100,000 for 25 years, should you die at any point during the 25 year term it would pay out the full £100,000. Where it provides a much greater level of cover the cost is significantly higher than Decreasing Life Insurance.

Do I Need Reducing Life Assurance?

To decide whether you need Decreasing Life Cover, ask yourself if you have any financial risk, such as a repayment mortgage or other debt. If the answer is yes then many people want to protect such debts should the worst happen.

If you take out Decreasing Term Life Insurance you can ensure that the debts you have are taken care of and not left to your loved ones after you die, potentially leaving them in financial hardship.

This could be especially important in the case of a mortgage on the family home, where your loved ones may have to give up the property if they cannot keep up with the mortgage after you’re gone.

Of all the Life Insurance products available Decreasing Term Insurance is generally the cheapest. This is because as the level of cover decreases over time the risk to the insurer is also declining; the longer the policy runs, the lower the payout the insurer will have to make in the event of a claim.

What Is The Risk Of Passing Away?

In our Health and Protection Survey we found out just how much we all underestimate the risk of death.

We are SIX times more likely to pass away before retirement than most people think

To help put things into perspective, using ONS Life Expectancy data we calculated the likelihood of death by the age of 60 for healthy people of the following ages:

This can help you understand the risks we all face in life and why so many people choose to protect themselves and their families with Life Insurance.

How Much Does Decreasing Life Insurance Cost?

The price of a Decreasing Life Insurance policy will vary from individual to individual depending on their circumstances.

The main personal factors that will be priced into the cost of a policy are:

- Your age

- Your state of health

- Your smoker status.

For example, if you are a 60-year-old smoker with a medical condition such as heart disease, your premiums will be a lot more expensive than a 30-year-old non-smoker who does not have any pre-existing health issues.

It is not just personal factors that will affect how much your insurance will cost but also your policy policy options.

- Level of Cover

The sum of money you would like to protect, the more you would like to cover the higher the monthly premiums will be.

- Length of Cover

The length of time you would like to be protected by the policy, the longer you would like to be covered the higher the risk of something happening and so the higher the monthly premiums.

- Include Critical Illness Insurance

In addition to paying out on death, the policy will pay out should you suffer a serious illness such as cancer, heart attack or stroke. Where the risk of suffering a critical illness is much greater it is reflected in significantly higher premiums.

Below are some sample monthly Decreasing Life Insurance premiums for £250,000 worth of cover over a 20 year period for a healthy individual of various different ages.

What's the Difference Between Level and Decreasing Life Insurance?

The difference between Level Life Insurance and Decreasing Term Insurance is how the benefit is treated over time.

Decreasing Life Cover as the name suggests, sees the benefit fall over time, reaching zero by the end of the policy’s term. This makes it particularly suitable for covering a straightforward repayment mortgage, where the outstanding debt also falls to zero by the end of the mortgage.

Make sure the interest rate assumed by your insurer / the policy doesn’t see your cover decrease faster than your mortgage, which could potentially leave you with a protection shortfall.

Level Life Insurance, on the other hand, sees the benefit remain fixed over time. This means that the amount you’ll receive if you die within the first year of the policy is the same as if you died in the last year of the policy.

A level policy is therefore more suited to covering an interest-only mortgage, where the outstanding capital balance doesn’t fall over time. It’s also well-suited to providing a constant level of family protection throughout the policy term.

Should I Add Critical Illness Cover?

Most Life Insurance policies offer you the option to include Critical Illness Insurance.

This means that the policy would not only pay out if you were to die, but also if you were to become critically ill as defined by the policy, i.e. developing a condition listed in the policy terms.

The main three illnesses are cancer, heart attacks and strokes, but Critical Illness Insurance tends to cover around 40 illnesses in total. However, there are policies which cover as few as 10 and policies that cover in excess of 100 illnesses, so it pays to make sure you read the policy carefully.

Adding Critical Illness Cover to your Decreasing Term Insurance policy will increase your premiums because there is a much greater risk of you suffering a serious illness than there is of you dying.

Your Critical Illness Cover will decline alongside your Life Insurance over the term of the policy, so you’ll get a lower payout in the later years of the policy term if you were to become critically ill.

Consider Income Protection

If there is a real need for protection against ill-health, we generally recommend you consider an alternative product called Income Protection. It pays out a monthly income should you be unable to undertake your own occupation for any illness or injury rather than limiting the cover to a specific list of serious illnesses.

The best Income Protection policies will pay out over the long-term, so until your retirement age, providing you with a regular income each month rather than a single lump sum. This prevents any issues where the lump sum is used up by repaying the mortgage and doesn’t leave you anything to live on, or it simply is depleted before you’re well enough to return to work.

What is Terminal Illness Cover?

Terminal Illness Insurance is different from Critical Illness Cover. Critical Illness Insurance is an optional add-on to Life Insurance designed to cover you if you become critically (and not necessarily terminally) ill.

Terminal Illness Cover, on the other hand, is built in to most Life Insurance policies as standard. You don’t pay anything extra for having it in place. Essentially, it just means that the policy will pay out early if you are diagnosed with a terminal illness and your life expectancy is 12 months or less.

Single or Joint Policy?

Of all the Life Insurance products, Decreasing Life Insurance is the perhaps most likely to be taken out as a Joint Life Insurance policy – many couples use it to protect a joint repayment mortgage.

However, whether it’s best to take out Decreasing Term Insurance on a joint basis will depend on what you want to protect.

This is because most joint policies are ‘joint life, first death’, which means that the policy will only pay out upon the death of the first person.

Although this type of policy can make sense for a couple who only want to protect their mortgage, if you want to do more with the payout than just pay off the mortgage, such as ensure children are taken care of, it may be more cost-effective to consider two individual policies.

Having two individual policies usually only comes at minimal extra cost to having a joint policy and effectively allows you to secure twice the payout, one on each death.

Should I Write the Policy into Trust?

When setting up a new Life Insurance policy, many people fall at the last hurdle and forget to write their policy into trust. Writing a policy into trust will protect your insurance benefit from inheritance tax and ensure that the full amount goes to your loved ones.

If you are intending for your Life Insurance benefit to go to your children, then writing your policy in trust is a very important step to take when you apply. However, you may not always need to write your policy into trust.

If you are using your Life Insurance policy to cover your mortgage, there may be less benefit to writing your policy into trust. This is because the insurance payout that is added to your estate would be used to pay off your mortgage debt, effectively ‘cancelling out’ any inheritance tax liability on the funds.

Advice on Decreasing Life Insurance

We are whole of market independent life insurance specialists. We live and breathe protection and it’s unlikely you can throw a question or scenario our way that we’ve not come up against before.

Why Speak to Us…

We started Drewberry because we were tired of being treated like a number and not getting the service we all deserve when it comes to things as important as protecting our health and our finances. Below are just a few reasons why it makes sense to let us help.

- There is no fee for our service

- We are independent and impartial

Drewberry isn’t tied to any insurance company, so we can provide completely impartial advice to make sure you get the most appropriate policy based solely on your needs.

- We’ve got bargaining power on our side

This allows us to negotiate better premiums for you than you going direct yourself.

- You’ll speak to a dedicated specialist from start to finish

You will speak to a named specialist with a direct telephone and email. No more automated machines and no more being sent from pillar to post – you’ll have someone to speak to who knows you.

- Benefit from our 5-star service

We pride ourselves on providing a 5-star service, as can be seen from our 4149 and growing independent client reviews rating us at 4.92 / 5.

- Gain the protection of regulated advice

You are protected. Where we provide a regulated advice service we are responsible for the policy we set-up for you. Doing it yourself or going direct to an insurer won’t provide this protection, so you won’t benefit from these securities.

- Claims support when you need it the most

You have support should you need to make a claim. The most important thing when it comes to insurance is that claims are paid and quickly. We are here to support you during the claims process and make sure it’s as smooth and stress free as possible.