Do I Need Mortgage Insurance?

Find out whether you need Mortgage Insurance. Read our 2024 guide, speak to our expert advisers and compare instant online quotes...

Receive an upfront cash lump sum for your loved ones to pay off the mortgage in full should you pass away during the term of your mortgage

Get My Instant Quotes

Receive an income to cover your monthly mortgage repayments should you be unable to work due to accident, sickness or unemployment

Get My Instant QuotesMortgage Insurance is split into two distinct products. Each type of policy covers very real – yet very different – risks.

How do you know which type of cover is right for you? And how can you tell whether you need Mortgage Insurance or whether you’ll be able to cope without it?

Mortgage Insurance is designed to cover:

Essentially, anyone with a mortgage needs to ask themselves if they could afford repayments if they couldn’t work due to accident, sickness, illness or injury.

If you’re considering Mortgage Life Insurance, ask yourself what’s protecting your family and their home in the event that you pass away.

It may feel like Mortgage Insurance is mandatory for a mortgage to be approved but that’s not the case. However, it does have a lot of benefits that make it a worthwhile protection product to consider.

If you’re injured or diagnosed with a serious illness such as cancer, you may need to leave work to receive treatment, potentially depriving your household of a primary earner.

As well as the risk of not being able to work due to accident or sickness, consider what would happen if you passed away. According to the Office for National Statistics, 11.2% of people who died in the UK in 2016 were aged between 20 and 60.

According to Drewberry’s Wealth & Protection Survey, 2 out of 5 people in the UK have no more than £1,000 in cash savings. Meanwhile, 44.9% of Brits have a mortgage and, of these, 1 in 4 still has at least £100,000 left to repay.

This would be an impossible debt for many families to repay in the event of the death of a loved one whose income contributed most to the mortgage repayments. It is why getting the right mortgage protection is such an important piece of financial planning.

While it might not be right for everyone, having some form of protection against illness or death should be a priority for homeowners – especially those with families. The right kind of protection insurance could defend against the worst, but the difficulty for most people is knowing exactly what cover meets their needs.

Mortgage Life Insurance is designed to pay out a lump sum to your beneficiaries to pay off the mortgage in full in the event of death or the diagnosis of a terminal illness. This usually means that your loved ones are able to stay in the home without worrying about keeping up with mortgage payments.

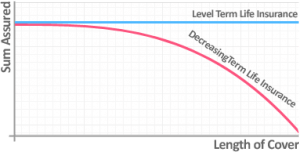

There are two types of Mortgage Life Insurance that you need to be aware of in order to find the right one for you:

They offer considerably different levels of cover, which is why it is so important that you know the difference between decreasing and level life insurance before you start shopping for policies.

If you’re living with a partner, you may also want to think about a Joint Mortgage Life Insurance policy (which is also known as Shared Mortgage Life Insurance). With this type of mortgage protection, your mortgage would be paid off in full should either of you die.

With a joint policy, if either you or your partner were to die while you have this policy, the insurer would pay out to the surviving person who would then use the payout to clear the mortgage.

It’s not always necessary to write Life Insurance into trust as the sum is destined for the mortgage lender, so the outstanding mortgage balance on the estate negates the lump sum received from the Life Insurance.

In other instances, it may simply offer more control to write the policy into trust – the process is free and Drewberry’s experts can facilitate it, so it might be something you want to consider regardless.

While Life Insurance plans pay out upon death or diagnosis of a terminal illness, Critical Illness Cover (CIC) will pay out if you develop a critical illness or injury.

If you have Mortgage Life Insurance with Critical Illness Cover, your plan will pay out for either death or a serious illness.

Critical Illness cover will pay out a tax-free lump sum if you are diagnosed with an illness that your insurer has specified. The three most common reasons for claiming on these policies are

According to our Wealth and Protection Survey, 43.8% of people said they’d rely on savings if they needed to take six months or more off work due to illness or injury. However, our survey has also found that 2 out of 5 people in the UK have no more than £1,000 in cash savings.

44.9% of British people have a mortgage and 1 out of 4 Brits still has at least £100,000 left on their mortgage.

If you only needed to cover your mortgage payments for a short time, Mortgage Payment Protection Insurance might be a good option. Given that it’s short-term, it tends to be among the cheaper methods of protecting your mortgage because claims are often capped to a maximum of 12-24 months.

Given the short payout length, it may not be enough to support you if you were to have a serious illness or injury that took you out of work for several years.

While Mortgage Payment Protection Insurance can kick in to keep up with your mortgage repayments if you can’t work due to accident, sickness or unemployment, it’s a short-term product. This could be problematic if you fell ill with a long-term condition.

For this reason, we generally recommend standard Accident & Sickness Insurance, also known as Income Protection Insurance, potentially alongside a standalone Unemployment policy if redundancy cover is required, as this could provide a more comprehensive protection for your circumstances.

When looking for the right Mortgage Insurance policy, there are a few things that you can look out for:

Why not use our Mortgage Insurance Calculator to compare the best UK insurers.

Once you’ve run your Mortgage Insurance quotes, you’ll have our expert advisers on hand to help you along the way, including advising you on the right policy, the right amount of cover, and how to tailor your policy to give maximum protection for minimal cost.

We started Drewberry™ because we were tired of being treated like a number.

We all deserve a first class service when it comes to issues as important as protecting our health and our finances. Below are just a few reasons why it makes sense to talk to us.

At Drewberry, we help our clients secure and protect potentially the most important investment in their life – their homes.

If you’re in need of advice just pop us a call on 01273646484 or email help@drewberry.co.uk.

Drewberry™ uses cookies to offer you the best experience online. By continuing to use our website you agree to the use of cookies including for ad personalization.

If you would like to know more about cookies and how to manage them please view our privacy & cookie policy.