What Is The UK's Best Income Protection Insurance ...

Read our 2024 Best Income Protection Insurance UK Guide, get expert regulated advice and compare online quotes from Aviva, Vitalit...

Income Protection Insurance is one of the most valuable protection products to purchase if you’re worried about how you would cope if you couldn’t work due to accident or sickness. For instance…

There are a lot of reasons people give for avoiding taking out Accident & Sickness Insurance. In the hopes that we may convince you to invest in this valuable protection product, we’ve busted some myths around the top 6 excuses that people use to avoid taking out Income Protection Insurance.

Many of us tend to have an optimistic outlook when it comes to our wellbeing, living by the mantra ‘it won’t happen to me’. However, most of the people out of work due to illness or injury probably thought the same.

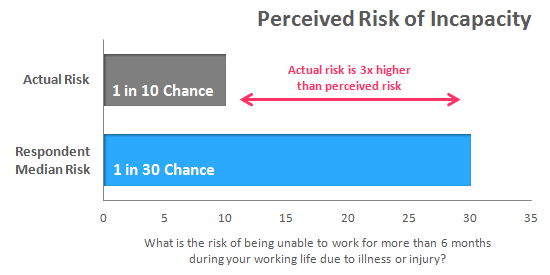

Our Protection Survey asked the public to estimate the chances of someone needing to be off work for more than 6 months due to ill health. The median result of our participants was that there is a 1 in 30 chance of needing more than 6 months off.

The real answer to this question, however, is that 1 out of every 10 people will need to take more than 6 months off during their working life to recover from an illness or injury. This means that the risk of being seriously ill or injured is 3 times higher than we perceive it to be.

There is a 1 in 10 chance that you will become severely injured or ill during your working life and require more than six months off of work. What you would do if the worst did happen and you were out of work for six months?

Following on from the points above, is it any wonder why Income Protection Insurance can be perceived as expensive if we all tend to underestimate the chances of needing to claim?

A suspicious mind might think that premiums are ‘expensive’ because insurers are making huge profits, but this generally isn’t the case given how competitive it is in the UK insurance market.

It’s important to remember that when setting the cost of your Income Protection premiums that there are a lot of factors you can do to keep a lid on costs. The cost of a policy won’t be the same for everyone and with a bit of research you will find that a lot of available Sick Pay Insurance options are more than affordable.

If you’re worried about the cost of Income Protection, there are some aspects of your policy that can be adjusted to reduce the cost of Income Protection:

The cost of your policy will also be affected by your own personal circumstances, such as your age, occupation, and your smoker status.

A common misconception that some people share is that insurers deny people’s claims quite frequently.

The truth is that insurers rarely reject Income Protection claims and, when they do, it’s often because of an issue that wasn’t disclosed at the application stage, or due to outright fraud.

In our survey, we asked 2,000 UK workers what proportion of insurance claims they thought were paid by the top five insurers. We were surprised when results showed that people think that only 50% of these insurer’s claims are paid when the reality is very different.

Insurers

| 2014

| 2015

| 2016

|

|---|---|---|---|

Holloway Friendly

| 96% | 96.9% | 98% |

British Friendly

| 96.7% | 97.8% | 97% |

Shepherds Friendly

| 96.7% | 97.6% | 97% |

Royal London

| 90% | 94% | 95.6% |

Legal & General

| 93.9% | 95% | 94.4% |

The Exeter

| 94% | 94% | 94% |

Cirencester Friendly

| 94% | 94% | 94% |

Vitality Life

| – | 96% | 94% |

Aviva

| 93.2% | 92.4% | 92.6% |

Liverpool Victoria

| 85% | 92% | 90% |

Zurich

| 93% | 87% | 85% |

Aegon

| 92% | 85% | 85% |

Income Protection claim payout rates have been consistently high among the top insurers. The top five insurers by claims payout rate all paid in excess of 94% of claims.

The amount of successful claims is considerably higher than what our survey participants expected them to be, which shows that there is very little cause to worry that your claim will be declined.

One of the top reasons for these rare occurrences of claims being rejected is people misunderstanding what is covered by their policy or not providing the correct information when they apply.

An adviser can help you avoid this by assisting with your application and explaining your policy to you clearly.

Samantha Haffenden-Angear

Independent Protection Expert at Drewberry

Employment & Support Allowance (ESA) is one potential source of income if you’re unable to work, but it’s very unlikely that you would live comfortably on benefits alone.

Depending on your circumstances, ESA will pay out an average of £84.80 per week. This can seem like an absurd amount to live on when you consider that the average UK household expenditure per week in 2016 was more than £500.

As you can see, for many people benefit payments could barely make a dent in their monthly expenditure, which is why Sick Pay Insurance is seen as a vital protection product for anyone that wants to protect their savings and income.

In 2016, the average length of Sick Pay Insurance claims for LV= was 7 years and 7 months and the average benefit payout was £14,695.

When deciding if you need Accident & Sickness Insurance, it is important to find out what your employer would provide you with if you needed to take time off of work due to illness or injury.

However, even where sick pay is offered by their employers, many people may find that their entitled sick pay is not sufficient to support them while they are out of work.

Statutory Sick Pay – the minimum an employer has to pay you – stands at a weekly rate of £109.40 for up to 28 weeks. Some employers won’t pay you anymore than this, and it’s clearly a very small amount.

Some employers will choose to go beyond this and provide a level of full sick pay for a period of time. However, our Protection Survey showed that 24% of people did not receive any additional sick pay from their employer and received only the national minimum.

As mentioned, if you do receive more sick pay than this, you can always increase your deferred period to lower the cost of cover.

Some people believe that the money you save by not buying Income Protection Insurance can be put in the bank instead and used when you’re low on income.

While it is always worthwhile to save money, there is a good chance that your savings won’t be enough to support you if you are incapacitated. If you fall ill after only one month of saved premiums, for example, you would struggle to get by.

Considering that average weekly expenditure for UK households exceeds £500, these statistics mean that…

2 out of 5 adults wouldn’t last any longer than two weeks if they tried to live on their cash savings without any other source of income.

On the other hand, by paying premiums of, for example, £50 per month, you could have almost immediate access to monthly payments of 50% to 70% of your regular income. That will leave you the option to secure the rest of your monthly savings for your retirement.

If you have been putting off purchasing Accident & Sickness Insurance for any of these reasons, then it may be time for you to reevaluate your situation.

Is Income Protection worth it? For most working adults it is one of the most valuable forms of protection ensuring you are well prepared if you ever faced misfortune of being unable to work and earn an income in the future.

We started Drewberry because we were tired of being treated like a number and not getting the service we all deserve when it comes to things as important as protecting our health and our finances. Below are just a few reasons why it makes sense to let us help.

If you would like to learn more or compare income protection quotes from the UK’s leading providers then please don’t hesitate to get in touch.

Pop us a call on 02084327333 or email help@drewberry.co.uk.

Tom Conner

Director at Drewberry

Drewberry™ uses cookies to offer you the best experience online. By continuing to use our website you agree to the use of cookies including for ad personalization.

If you would like to know more about cookies and how to manage them please view our privacy & cookie policy.